Unlocking Insights: Dive Deeper into Housing Needs with New Dashboard and Video Series

Oct 15, 2024

CHFA and the Partnership for Strong Communities have partnered on an HNA explainer video series covering

the major themes of the CHFA Housing Needs Assessment.

As a major industry partner, CHFA seeks to continuously respond to the housing needs of our residents. To do so, we must stay abreast of key market trends, world events, and economic conditions that impact Connecticut families. In this way, we better position ourselves to serve our communities by creating programs and solutions that address these challenges. In late 2023, CHFA published its second Housing Needs Assessment (HNA). The goal of the HNA is to provide as close to real time data as possible for CHFA and its partners to make informed data-driven decisions.

It’s been roughly one year since the publication of the 2023 Housing Needs Assessment, and we wanted to provide an update on how the Connecticut housing market has changed over the last year.

We’re also excited to bring the HNA to life with an interactive Dashboard. The data contained in the dashboard will be updated regularly and aims to provide our partners with live and interactive data.

For questions or requests for additional data, please email research@chfa.org?.

So what's new since last year's HNA?

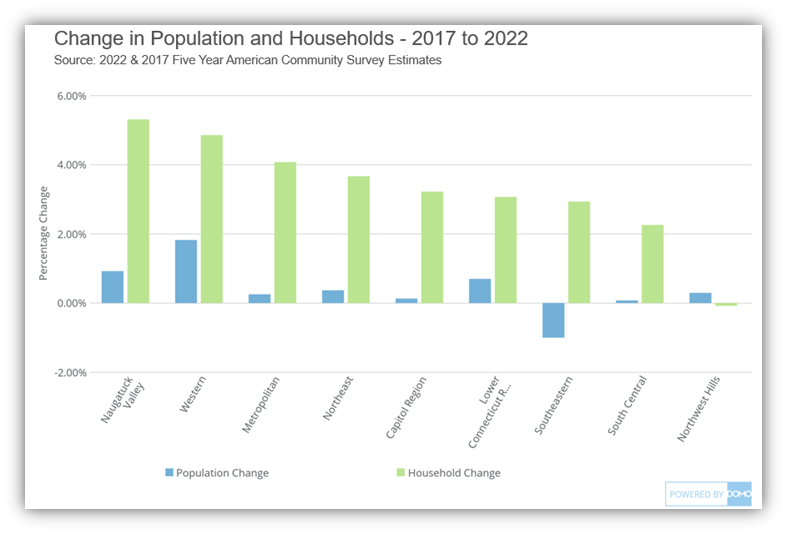

Household formation in Connecticut remains strong even as population growth is moderate. According to the U.S. Census, a household is formed any time someone occupies a housing unit. For example, household formation occurs when a recent college graduate moves from their parent’s house into a place of their own. Between the 2017 and 2022 Five Year ACS periods, Connecticut saw a 3.53% increase in the number of households with a population increase of just 0.47%. This trend in household growth was strong across the state with each of the nine planning regions seeing an increase of more than two percent. This phenomenon points to both an increased demand for housing and suggests that households are getting smaller. Over the same Census period, the average household size in Connecticut dropped slightly from 2.55 to 2.48.

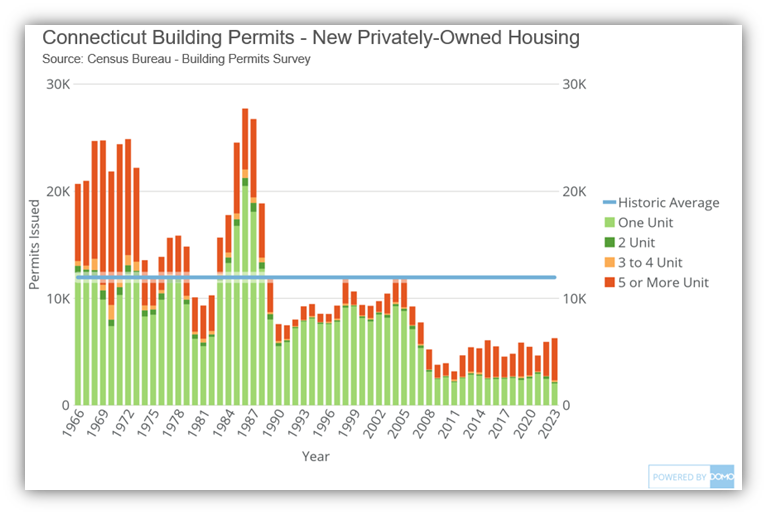

According to the U.S. Census Building Permits Survey, in 2023 there were roughly 6,300 permits issued for new privately owned units in Connecticut, the highest number since 2007 but still well below Pre-Great Recession levels. However, permits for units in structures with five or more units jumped to roughly 3,900, the highest since 1988. On the other hand, permits for one-unit buildings declined to just over 2,000, in 2023, the lowest since the survey began in 1966.

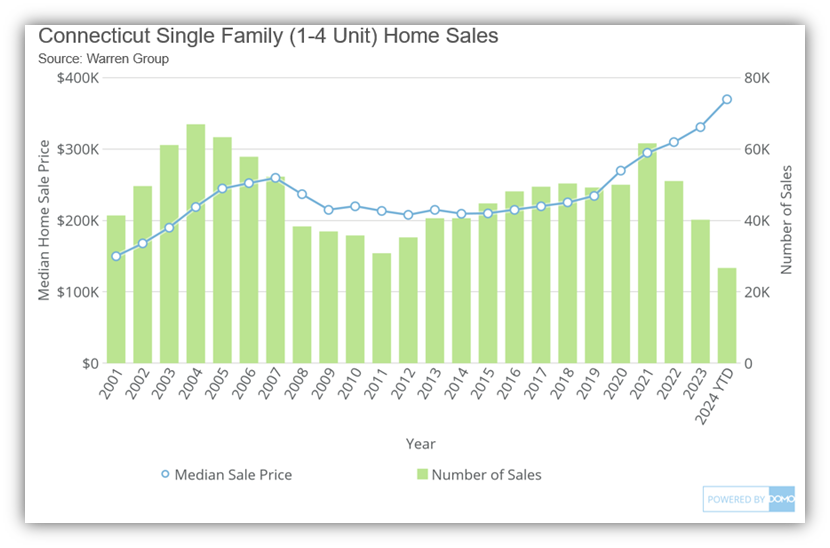

In 2021, Connecticut saw nearly 62,000 single-family home (1 to 4 units) sales, the highest number since 2005. While total sales have slowed in recent years, the median sale price in Connecticut has continued to increase from $234,500 in 2019 to $331,000 in 2023, a 42% increase.

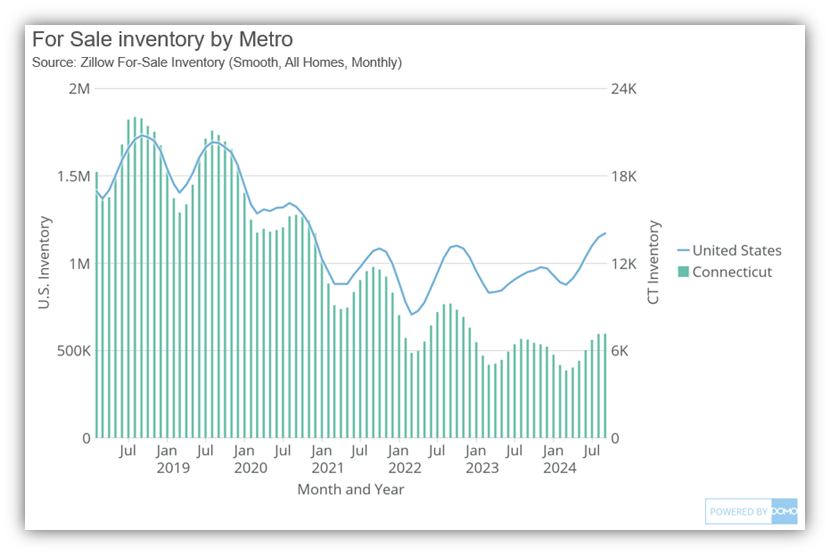

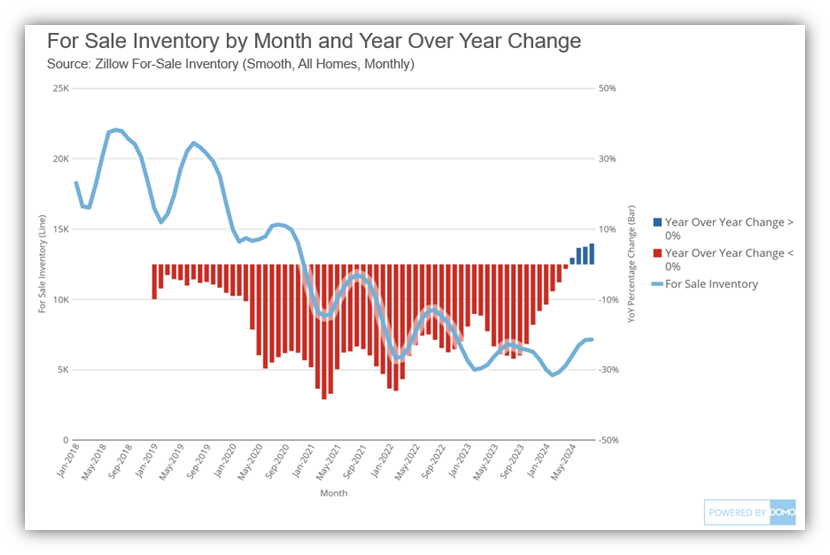

Every year, for-sale inventory levels operate in a cyclical nature, growing in early spring, peaking in summer, and ebbing in the fall and winter months when the school year and holidays dissuade people from moving. With the onset of the pandemic, Connecticut did not see the same seasonal increase in inventory as seen in previous years. As of August 2024, Connecticut had roughly 7,100 homes listed for sale, just 34 percent of the for-sale inventory in August 2019.

In recent months, Connecticut has seen some positive year over year growth in its inventory levels. Inventory levels in August 2024 were 6% higher than a year ago.

Decreased inventory, combined with increased household formation and homeownership demand among millennials, resulted in a dramatic uptick in the percentage of listings sold above their asking price. Prior to March 2020, only about 20% of home listings sold above their original asking price on average across all counties. During the pandemic period, that number grew to over 50% on average, with some markets in Connecticut reaching above 70% depending on the month and market. Interestingly, despite cooling across U.S. markets, Connecticut’s share of listings sold above asking price has remained higher than the U.S., indicating the state’s market has remained hotter than the country at large. As of July 2024, about 35% of all U.S. home sales sold above list price compared to 68% in Connecticut.

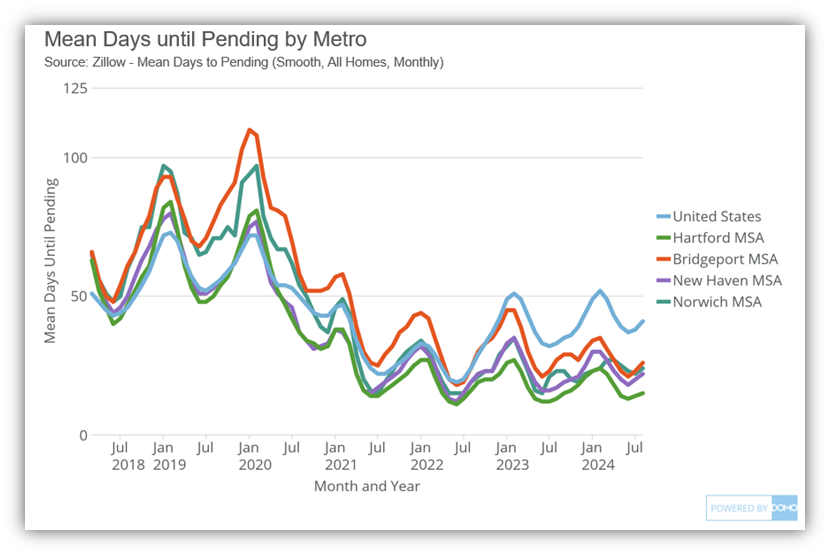

While home values and sales prices have increased over the course of the pandemic, so has the competition for listings. Across all of Connecticut’s markets, the average number of days a home is listed has decreased significantly. For example, in the Hartford Metro-Statistical Area (MSA), the average number of days between list date and sale pending date was 15 days in August 2024, down from an average of 48 days in August 2019.

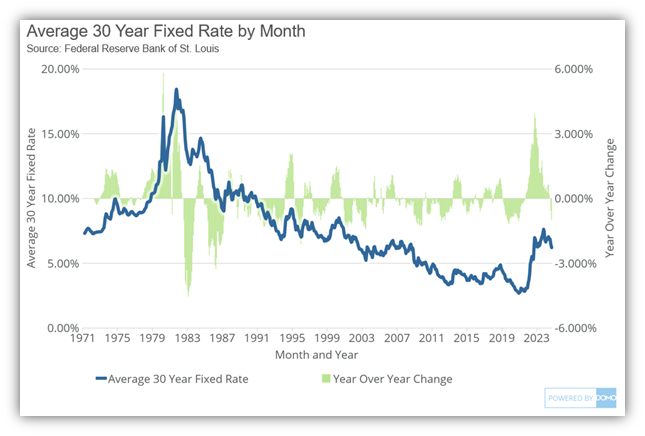

Additionally, as the Federal Reserve attempts to combat inflation, higher interest rates have further limited options for homebuyers. Between October 2021 and October 2022, the average 30-year fixed rate mortgage rate increased by 3.91 percentage points according to Freddie Mac. This increase represents the largest year-over-year increase in mortgage interest rates since 1981 and is creating further affordability challenges for homebuyers. According to Harvard’s Joint Center for Housing Studies (JCHS), nationwide “In April 2021, a household had to earn at least $79,600 a year to afford payments on the median priced home of $340,700. One year later, the income requirement stood at $107,600.”

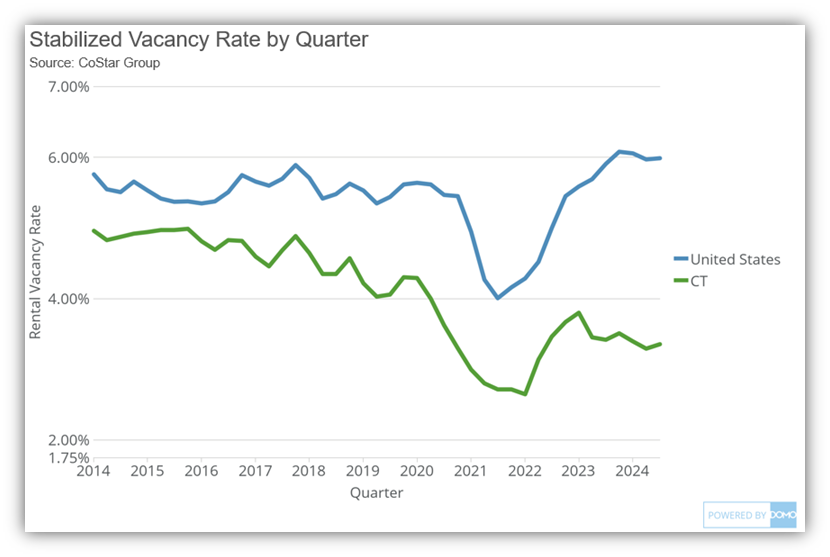

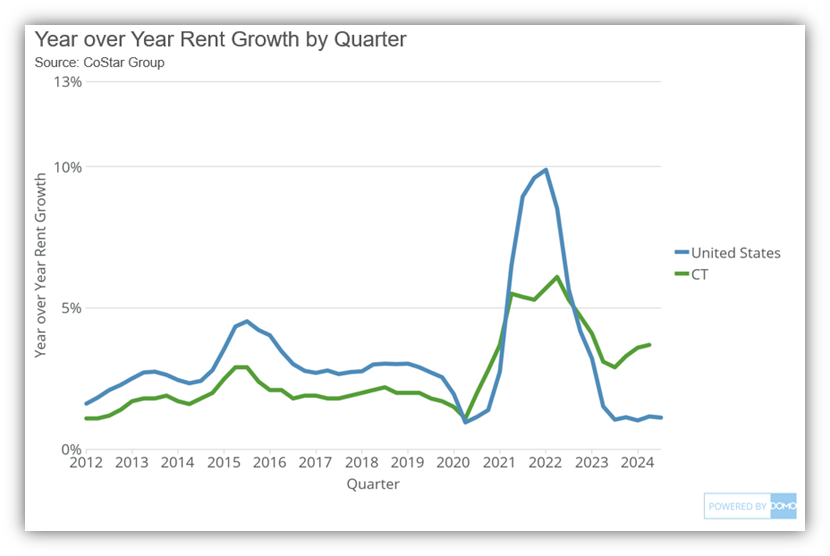

The pandemic also had dramatic effects on the rental market. Driven by strong demand for units and a competitive home sales market, rental vacancy rates in every Connecticut metro area dropped significantly in 2020. For example, in the Norwich metro-area the rental vacancy rate dropped from 5.71% in the Q2 2020 to 2.40% in Q3 2022.

Consequently, this scarcity pushed rents higher as households competed for fewer available units; Norwich Metro-area rents were up nearly 12% year-over-year in Q2 2022 according to CoStar. Rent growth have slowed in recent months however average asking rents in Connecticut are now well above pre-pandemic levels, up roughly 20% between Q2 2019 and Q3 2024.

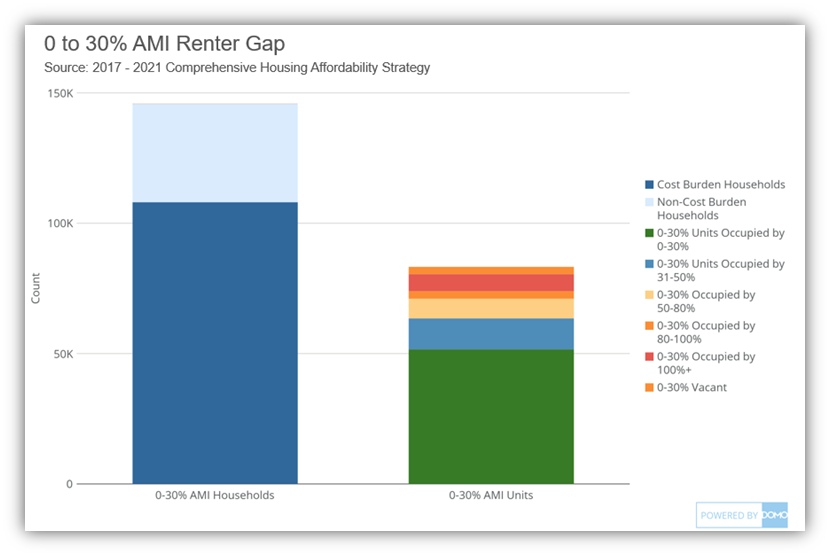

A key component of the Needs Assessment is the Housing Gap Analysis which attempts to estimate the number of units that need to be made available for a segment of renters or owners to have the necessary affordable housing options. It is generally accepted that a household is said to be “cost burdened” when it pays more than 30% of its income on housing. Thus, anything over this 30% marker is considered unaffordable. The Housing Gap Analysis indicates the number of additional housing units by tenure and affordability that are needed for the housing inventory to match the number of households at their respective incomes bracket based on Area Median Income (AMI) established by HUD.

Comprehensive Housing Affordability Strategy (CHAS) data, which is a custom tabulation of American Community Survey data for use by HUD, was used in the analysis. CHAS data provides a count of units and households by income bracket and tenure including occupancy data in a given geographic area. For the gap to be equal to zero in any given bracket, all households in a group must occupy a unit that is affordable at their income (e.g., a 30% AMI household lives in a unit affordable to a 30% AMI household). Factors that contribute to the gaps caused by a mismatch between households and units include:

- and/or Having households outside of a particular income bracket residing in units meant to be affordable for that particular bracket (e.g., 1,000 households and 1,000 units for a particular bracket but 500 of the units are occupied by households outside the bracket leading to only 500 units available to the 1,000 households).

- Having more households than units in a particular bracket (e.g., 1,000 households but only 500 affordable units available);

The Gap Analysis allows us to ask the question: “Are there enough units affordable to all Connecticut households?” As one might expect, the answer is no. Therefore, the next step is to assess both how many households exist in each income bracket and how many units are available to those households. We also evaluate the extent to which higher or lower income households occupy housing that is more or less expensive than what they can afford.

The graphic above uses the latest CHAS data released in September of this year. Extremely low-income (renters earning under 30% AMI) renters in Connecticut face the clearest need for additional affordable units. Roughly three quarters of these households are cost burdened as they face a significant lack of affordable options. There are significantly more households at this income level than there are units affordable to them. Additionally, of those units, 34% are occupied by households at a higher income level. These two phenomena combine to create a statewide “gap” of roughly 91,000 units. This gap is not a production target, but rather the number of units that would be needed to ensure households at the lowest income level have an affordable housing option.

****

Andrew Bolger is a Senior Research and Data Analyst in the Connecticut Housing Finance Authority’s Research, Marketing, and Outreach Department. In this role he manages CHFA’s housing database, tracks and analyzes housing market conditions, and evaluates CHFA programs. He received a BA in Economics and Political Science and an MA in Public Policy from the University of Connecticut.